Even seasoned brokers know the frustration of incomplete property data derailing a deal. Inaccurate or missing numbers can lead to flawed models and put client trust at risk. By mastering advanced modeling techniques and risk analysis, you position yourself as the go to expert for high-stakes property evaluations. Discover how organized data collection, dynamic proforma modeling, and KPI-driven analysis empower your presentations and move deals forward with confidence.

Table of Contents

- Step 1: Collect Key Property And Financial Data

- Step 2: Build Dynamic Proforma And Scenario Models

- Step 3: Evaluate Cap Rates, Valuations, And Kpis

- Step 4: Validate Results Through Sensitivity Analysis

Quick Summary

| Key Insight | Explanation |

|---|---|

| 1. Gather Accurate Property Data | Collecting thorough property fundamentals prevents miscalculations and enhances decision-making. Essential data includes rent rolls and lease agreements. |

| 2. Create Dynamic Proforma Models | Use actual market data to project cash flows and assess investment viability under different scenarios, ensuring flexibility in assumptions. |

| 3. Perform Cap Rate Analysis | Understanding cap rates helps evaluate investment profitability. Compare your cap rate to market comps to identify value or risk. |

| 4. Conduct Sensitivity Analysis | Test the impact of variable changes, like rent growth or occupancy rates, on returns to identify deal vulnerabilities and thresholds. |

| 5. Validate with KPI Tracking | Monitor key performance indicators such as IRR and cash-on-cash return to ensure the investment meets your financial objectives throughout the analysis. |

Step 1: Collect key property and financial data

You can't analyze a deal without solid information. This step is about gathering everything you need before you start modeling, so you're working with actual numbers, not guesses.

Start with the property fundamentals. You need square footage, unit mix, occupancy rates, and lease expiration schedules. Pull the most recent property appraisal or valuation report. Get the current rent roll, showing what each tenant pays and when their leases end. If you're analyzing a multifamily or office building, understand the tenant profile and any major lease rollovers coming up.

Next, gather the financial documentation. Request the last 3 years of tax returns and operating statements (P&Ls) from the seller or current owner. These show actual revenue and expenses, not projections. Look for:

- Gross rental income and any other revenue streams

- Operating expenses broken down by category

- Capital expenditure history

- Debt service, if the property is currently leveraged

- Tenant allowances or concessions already given

Don't skip the lease agreements. Review key tenant leases to confirm renewal dates, rent escalation clauses, and any renewal options. A tenant with a renewal option at below-market rates changes your 10-year underwriting entirely. Identify which tenants represent concentration risk—if one tenant is 40% of income and leaves, your deal falls apart.

Incomplete data leads to incorrect assumptions, which leads to bad decisions. Spend time upfront verifying everything before you model.

Collect market data relevant to your analysis. Get recent comparable lease rates for similar properties in the submarket. Pull market reports on absorption rates, vacancy trends, and growth forecasts. This data directly impacts your rent growth assumptions and tenant renewal risks.

Gather any physical or environmental reports. Get the Phase I environmental assessment, structural engineer's report if available, and any recent property inspections. These reveal hidden costs that kill deals if you're not careful.

Finally, understand the current capital structure. If the property is leveraged, get loan documents showing the debt amount, interest rate, maturity date, and prepayment terms. This affects how you model refinance risk and exit scenarios.

Organize this information in a single location where you can reference it throughout your analysis. Tools like DealCrunch.ai let you input and organize these details directly into your underwriting model, so everything stays connected.

Here's a quick reference to core data sources and their impact when evaluating a property deal:

| Data Source | Business Impact | Typical Risk if Missing |

|---|---|---|

| Property Appraisal | Reveals value and condition | May misprice deal or overlook issues |

| Rent Roll | Clarifies current income | Misses lease expiration risks |

| Financial Statements | Details actual performance | Can misestimate cash flows |

| Market Comparables | Guides rent and price assumptions | May misjudge market value |

| Environmental Reports | Identifies hidden liabilities | Could miss costly remediation |

| Loan Documents | Sets leverage and debt terms | Underestimates refinance risk |

Pro tip: Create a simple checklist of required documents before you request anything from the seller. Most brokers know what you need—a clear checklist just speeds up the process and signals you're organized and professional.

Step 2: Build dynamic proforma and scenario models

Now you transform raw data into actionable financial projections. A proforma model shows you what the deal actually looks like over time, and scenario modeling lets you test what happens when things change.

Start by building your base case proforma. This is your most likely outcome based on current market conditions and the property's fundamentals. The proforma combines income, expenses, and cash flows into one integrated model that shows how the investment performs year by year.

Your proforma needs several key components:

- Rental income projections based on current rents, market growth, and lease expirations

- Operating expenses including utilities, insurance, maintenance, and property management

- Capital expenditures for replacements and upgrades you anticipate

- Debt service if the deal is leveraged

- Cash flow to equity showing what investors actually receive

Understanding how to structure a real estate proforma helps you build one that captures all these moving pieces accurately.

Once your base case is solid, build scenario models to stress-test your assumptions. Create a bull case where rents grow faster and expenses come in lower. Create a bear case where rent growth slows and vacancy increases. Create a realistic worst-case scenario based on what could actually happen in your market.

Scenario modeling shows you the range of possible outcomes. You might find your base case is still profitable even if three tenants leave early or rent growth drops to 2% instead of 3%. Or you might discover that a single variable—like a major tenant departure—kills returns. This is valuable information before you commit capital.

Scenarios aren't guesses. They're stress tests based on market data and lease terms you already collected.

Build your models to be dynamic and flexible. Use formulas that automatically update when you change assumptions, so you can quickly test different scenarios without rebuilding from scratch. If you increase rent growth from 2% to 3%, the entire model should recalculate instantly.

Make sure your models output the metrics that matter for your analysis. You need cap rate, internal rate of return (IRR), equity multiple, cash-on-cash return, and net present value. Different investor types care about different metrics, so your model should calculate all of them.

Pro tip: Build your base case conservatively. Use market data you can defend, not optimistic assumptions. When you present to investors, conservative base cases with realistic upside scenarios outperform models where the base case already assumes everything goes perfectly.

Step 3: Evaluate cap rates, valuations, and KPIs

Your proforma generates numbers, but you need to know what those numbers actually mean. This step is about evaluating whether the deal makes sense relative to the market and your investment criteria.

Start with cap rate analysis. The cap rate tells you what annual return the property generates on your investment. Calculate it by dividing net operating income by purchase price. A 5% cap rate means the property produces 5% annual returns based on current income.

Cap rates reflect market conditions and risk. How cap rates function as valuation metrics helps you understand what drives them up and down. Interest rates, tenant quality, property age, and market competition all influence what cap rate a property trades at. A newer office building in a strong market might trade at 4%, while an older retail property in a declining area might be 7%.

Compare your deal's cap rate to comps in the market. If similar properties are trading at 5% and yours is 6%, that spread signals either higher risk or better value. Ask why. Is it a different tenant profile? Different lease terms? Different location? Understanding the why matters more than the number itself.

Evaluate your valuation assumptions. Look at your exit cap rate, which is what you assume the property will be worth when you sell. Most brokers assume the exit cap rate is similar to entry cap rate, but market conditions could shift. Build sensitivity tables showing how returns change if you exit at different cap rates.

Track these KPIs throughout your analysis:

- Net operating income growth year over year

- Cash-on-cash return in year one and stabilized year

- Internal rate of return (IRR) over your hold period

- Equity multiple (total cash returned divided by cash invested)

- Debt service coverage ratio (cash flow relative to debt payments)

- Loan-to-value ratio and how it affects leverage risk

Cap rates compress in strong markets and expand in weak ones. Your assumptions about where rates are heading directly impact deal returns.

Understanding the determinants of retail cap rates shows how tenant risk, market specifics, and property characteristics shape what investors actually pay. This research applies across property types and helps you spot when a deal is mispriced.

Build your own KPI dashboard showing all metrics side by side. Compare your deal to your underwriting guidelines and historical performance. If your IRR target is 15% and this deal only generates 12%, you need to understand why before moving forward.

Use this summary table for key investment performance metrics and their value:

| KPI | What It Measures | Why It Matters |

|---|---|---|

| Cap Rate | Income-to-value efficiency | Signals market risk and pricing |

| IRR | Time-adjusted returns | Shows deal profitability |

| Cash-on-Cash Return | Annual cash yield | Tracks investor income |

| Equity Multiple | Total cash returned/share | Measures total investment gain |

| Debt Service Coverage | Cash flow vs. debt payment | Assesses loan repayment safety |

Pro tip: Cap rates don't tell the whole story. A high cap rate can signal great value or hidden risk. Always dig into why the cap rate is where it is, and never rely on cap rate alone to make your decision.

Step 4: Validate results through sensitivity analysis

Your proforma shows what happens if everything goes according to plan. Sensitivity analysis shows what happens when it doesn't. This step protects you from overlooking risks that could derail returns.

Sensitivity analysis tests how changes in key assumptions impact your outcome metrics like IRR and equity multiple. You're essentially asking: if rent growth is 1% instead of 2%, or if occupancy drops from 95% to 85%, how much do my returns change?

Start by identifying your most critical assumptions. These are the variables with the biggest impact on returns. For most deals, the heavy hitters are:

- Rental rate growth annually

- Exit cap rate at sale

- Occupancy and vacancy rates

- Operating expense growth

- Major tenant departures or renewal rates

- Debt terms and refinance assumptions

Build a one-variable sensitivity table for each critical assumption. Show how your IRR changes as you adjust that variable up and down by increments. If you assume 3% rent growth, test what happens at 1%, 2%, 3%, 4%, and 5%. Most deals have a breaking point where returns collapse.

Then build two-variable sensitivity tables combining your two biggest risk factors. This might be rent growth and exit cap rate, or occupancy and operating expenses. Two-variable tables show you how sensitive returns are when multiple things change together, which is more realistic.

Create visual charts showing your sensitivity results. A heat map showing IRR at different rent growth and cap rate combinations is easier to understand than a table of numbers. Your audience sees instantly where the deal gets risky.

If your deal only works if three perfect things happen simultaneously, that's not a good deal. You need returns that hold up when assumptions slip.

Test the downside scenarios you already modeled. Run sensitivity analysis on your bear case to see how much additional stress it can handle. If the bear case IRR is already 8%, small additional changes won't kill the deal. If it's 6%, you're closer to trouble.

Identify your deal breakers. Every broker has a minimum IRR, minimum cash-on-cash return, or maximum leverage threshold. If a 2% deviation in rent growth kills the deal, that's a warning sign. You need cushion for the real world.

Use tools that automate sensitivity analysis so you can test quickly. Manual sensitivity tables in spreadsheets are slow and error-prone. Automated models let you test dozens of scenarios in minutes.

Pro tip: Present sensitivity analysis to investors alongside your base case. Show them the realistic range of outcomes, not just best case. Investors trust brokers who acknowledge risks and stress-test assumptions thoroughly.

Master Commercial Real Estate Deal Analysis with Confidence

The article highlights the critical need for comprehensive data gathering, dynamic proforma modeling, and rigorous sensitivity testing to uncover the true potential and risks of commercial real estate deals. If you are a broker, investor, landlord, or tenant, you know how challenging it is to organize complex financials and market data while running multiple scenario analyses. Key pain points include avoiding underwriting errors, managing fluctuating cap rates, and stress-testing assumptions to ensure resilient returns.

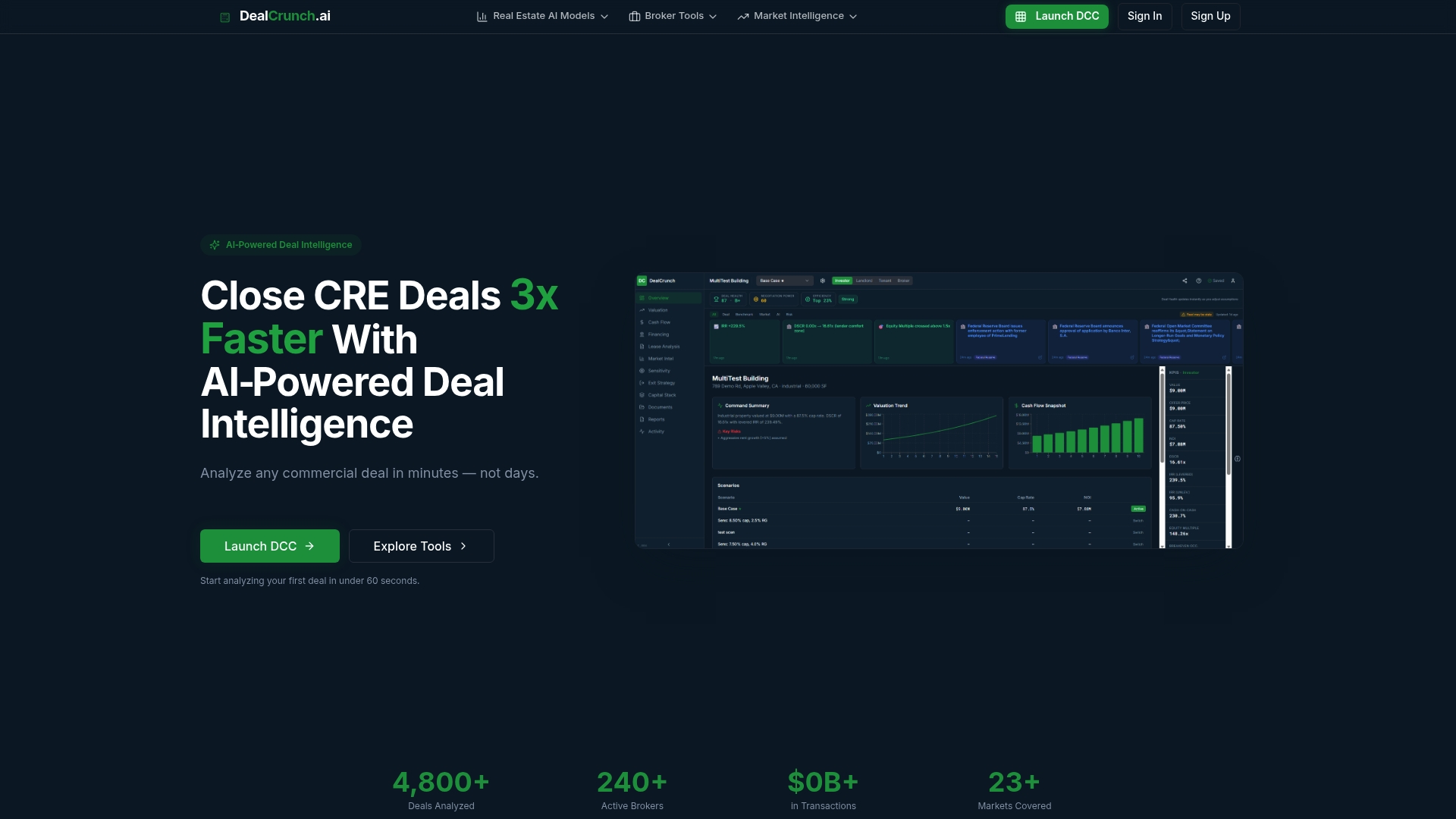

DealCrunch.ai solves these challenges by providing an all-in-one AI-powered platform designed to replace fragmented spreadsheets and manual calculations. From 10-year proforma modeling and cap rate analysis to scenario comparison engines and deal health scoring, everything seamlessly connects so you can verify your data, model dynamic outcomes, and validate investment KPIs with ease. Save time, reduce risk, and present your deals more professionally with advanced tools that keep pace with today’s fast-moving CRE markets.

Ready to elevate your deal analysis process and gain institutional-grade insights that drive smarter decisions?

Explore how DealCrunch.ai helps you organize key property data, build flexible models, and perform sensitivity analysis all in one place. Start transforming your underwriting approach today by visiting our AI-powered commercial real estate analysis platform. Don’t wait until risks blindside your deal returns - act now and uncover every opportunity before your next deal closes.

Frequently Asked Questions

What key data should I collect before analyzing a commercial real estate deal?

To analyze a commercial real estate deal successfully, gather key property and financial data including square footage, occupancy rates, lease expiration schedules, and at least three years of financial statements like operating statements and tax returns. Organize this information in a single location to streamline your analysis process.

How can I build a proforma model for a commercial real estate deal?

Start by creating a base case proforma that includes projected rental income, operating expenses, capital expenditures, and debt service. Use this model to visualize cash flows year by year, ensuring your assumptions are realistic and defensible.

What is sensitivity analysis, and why is it important in real estate analysis?

Sensitivity analysis tests how changes in key assumptions, like rental rate growth or occupancy rates, impact your return metrics. By identifying your most critical assumptions and evaluating their impact, you can uncover potential risks and ensure your deal remains viable under different scenarios.

How do I calculate the cap rate for a commercial property?

Calculate the cap rate by dividing the property's net operating income by its purchase price. This metric provides insight into the property's return on investment relative to its value and aids in comparing deals against market rates.

What key performance indicators (KPIs) should I track in commercial real estate?

Track KPIs like Net Operating Income growth, Cash-on-Cash return, Internal Rate of Return (IRR), and Debt Service Coverage Ratio. Monitoring these metrics helps you assess the deal's performance against your investment criteria throughout your analysis journey.